Published by

Gold Expert

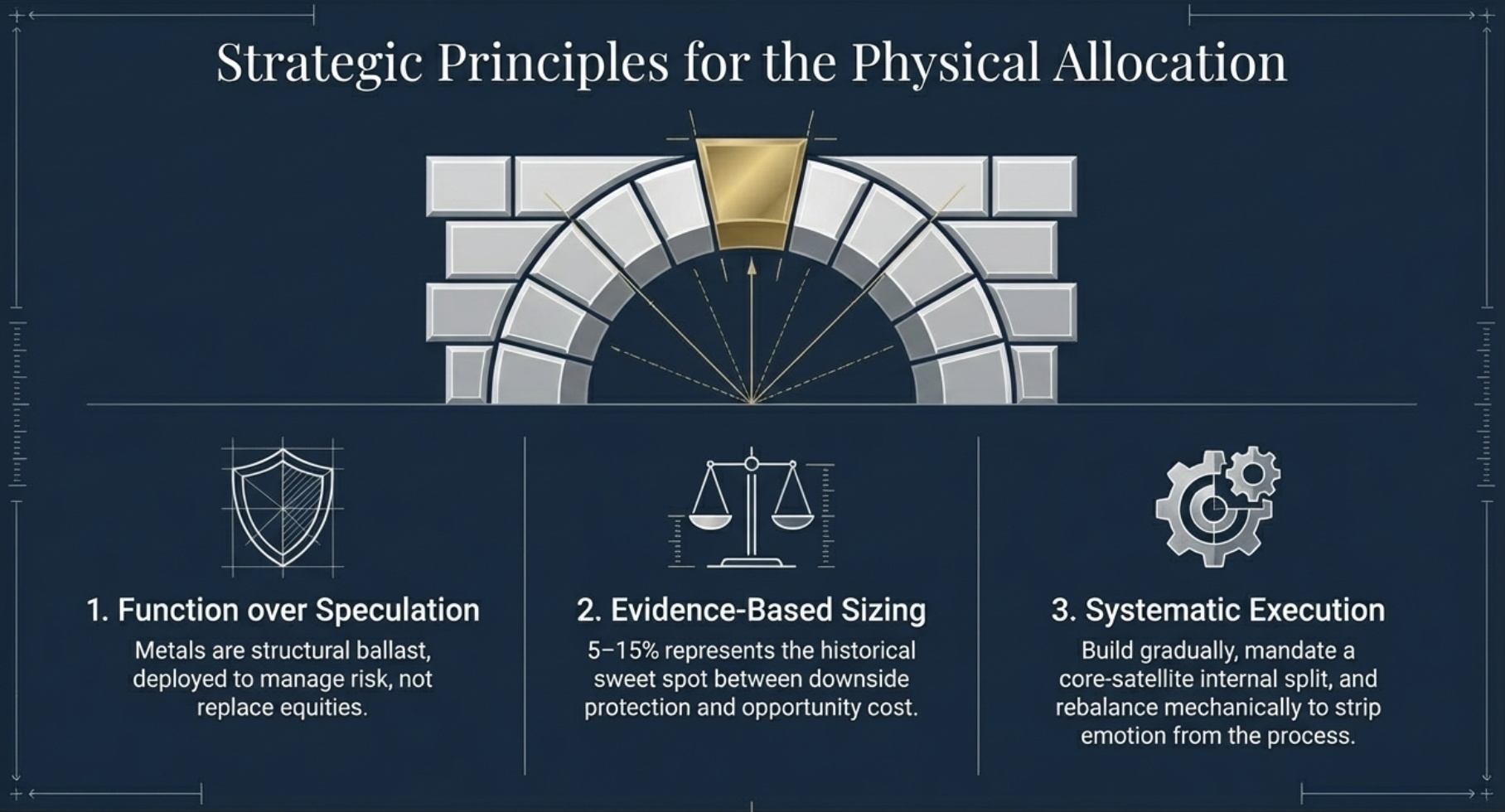

TL;DR

- There is no single “correct” percentage of your portfolio that must be in gold and silver; ranges like 5–15% are starting points, not hard rules.

- Gold tends to help most in inflationary or crisis periods, while stocks usually dominate in long bull markets and bonds handle income—when they still diversify.

- Your ideal gold and silver allocation depends on your risk tolerance, time horizon, liquidity needs, and how you expect inflation and markets to behave.

- A gradual, rule‑based approach (build over time, rebalance, stay in a comfort range) usually works better than reacting to headlines.

- Think of metals as one tool alongside stocks, bonds, and cash to shape your overall risk and resilience—not as a standalone “solution.”

How much gold and silver is “enough”?

You can think of “enough” gold and silver as the amount that clearly improves your portfolio’s resilience without compromising your ability to grow, earn income, or access cash when needed. Put differently: you want enough precious metals to notice during inflation or crises, but not so much that you’re stuck if you need money or miss equity growth for a decade.

Ranges like 5–15% of your total portfolio in precious metals are common because many studies and practitioners find that level can improve diversification, but those numbers are reference points, not commandments. Your personal “enough” might be below or above those ranges depending on your situation and preferences.

Key concepts: allocation, diversification, and risk

What we mean by “allocation”

When we talk about gold and silver allocation, we mean the share of your overall investable assets held in physical precious metals (and possibly metal‑linked instruments), not the size of your last purchase. If your total portfolio is $100,000 and you own $8,000 in bullion and coins, your precious metals allocation is 8%.

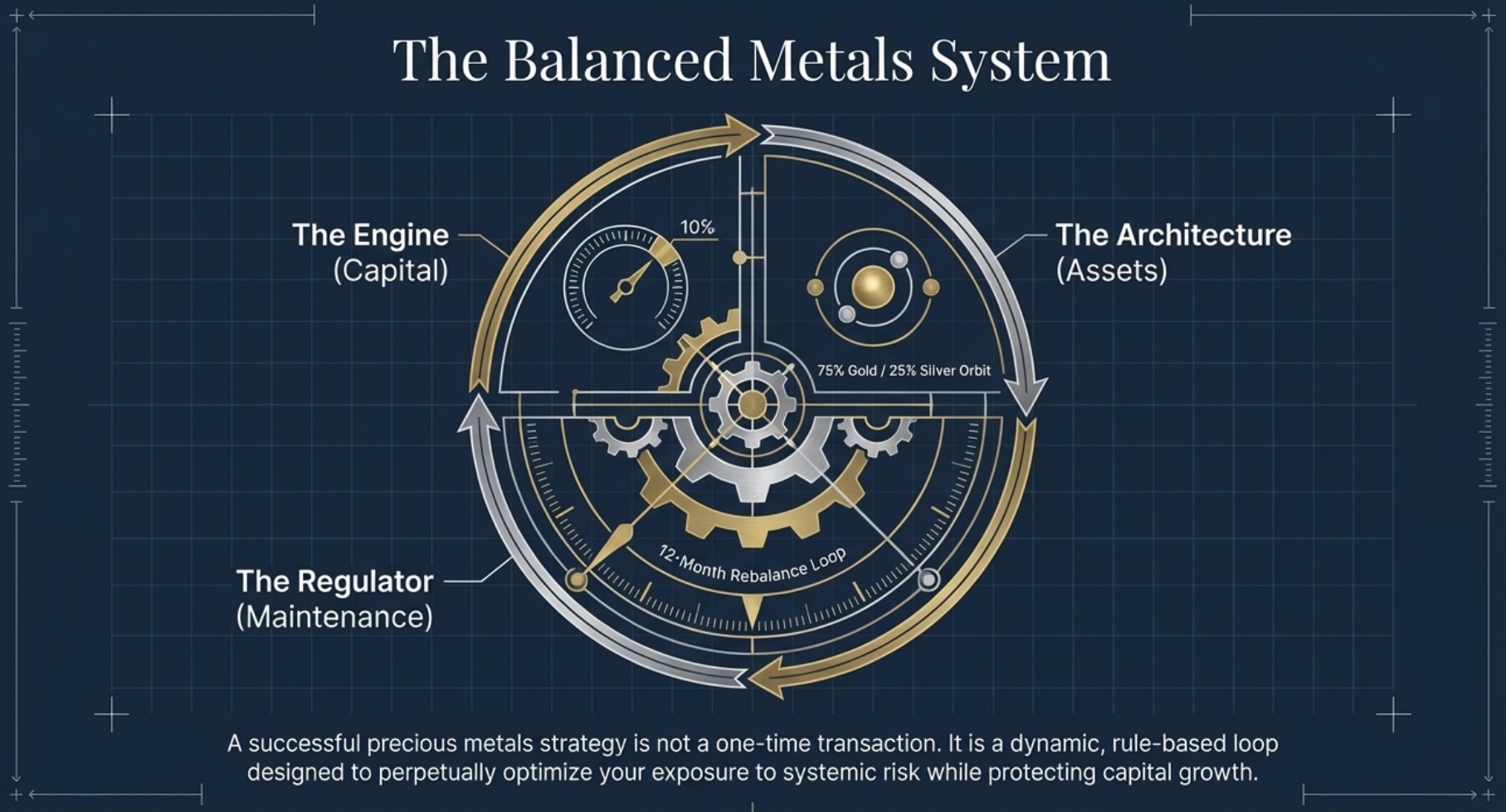

It is most useful to think about this allocation over multi‑year cycles rather than reacting to monthly price swings. The goal is to define a target range that matches your risk profile (for example, 5–10% or 8–12%) and stay roughly inside it, rebalancing occasionally as prices and your life change.

Is gold a good investment in a portfolio?

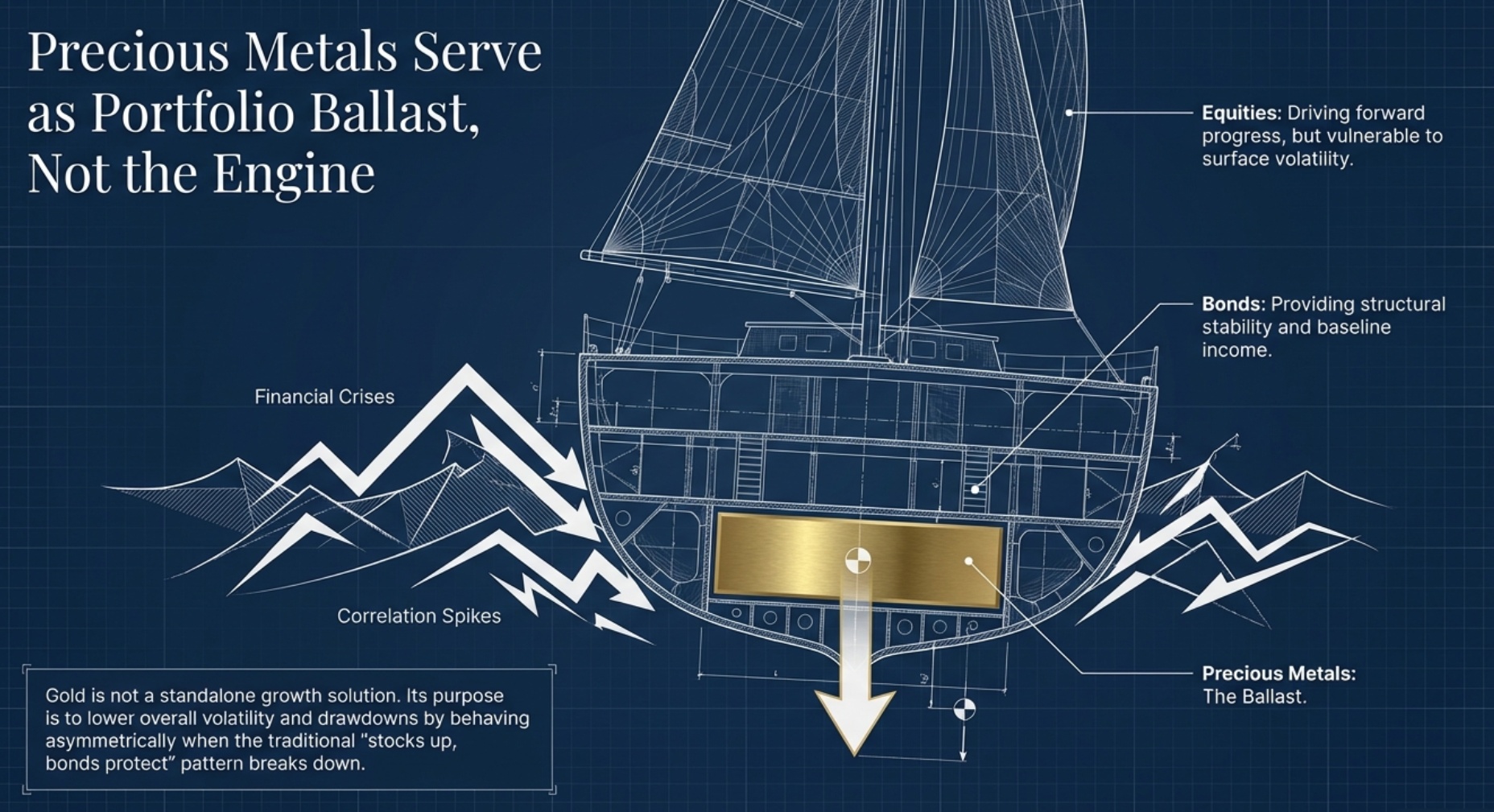

In a diversified portfolio, gold is generally better viewed as a risk‑management tool than as a primary growth engine. Academic and practitioner research shows that adding some gold can lower overall volatility and drawdowns because its returns often move differently than stocks and, increasingly, than bonds.

Over very long periods, equities have delivered higher expected returns than gold, but gold has tended to shine during specific regimes—especially high inflation, policy uncertainty, and certain crisis environments—when stocks and bonds can struggle together. That asymmetric behavior is why many evidence‑based frameworks treat gold as a strategic diversifier rather than a speculative side bet.

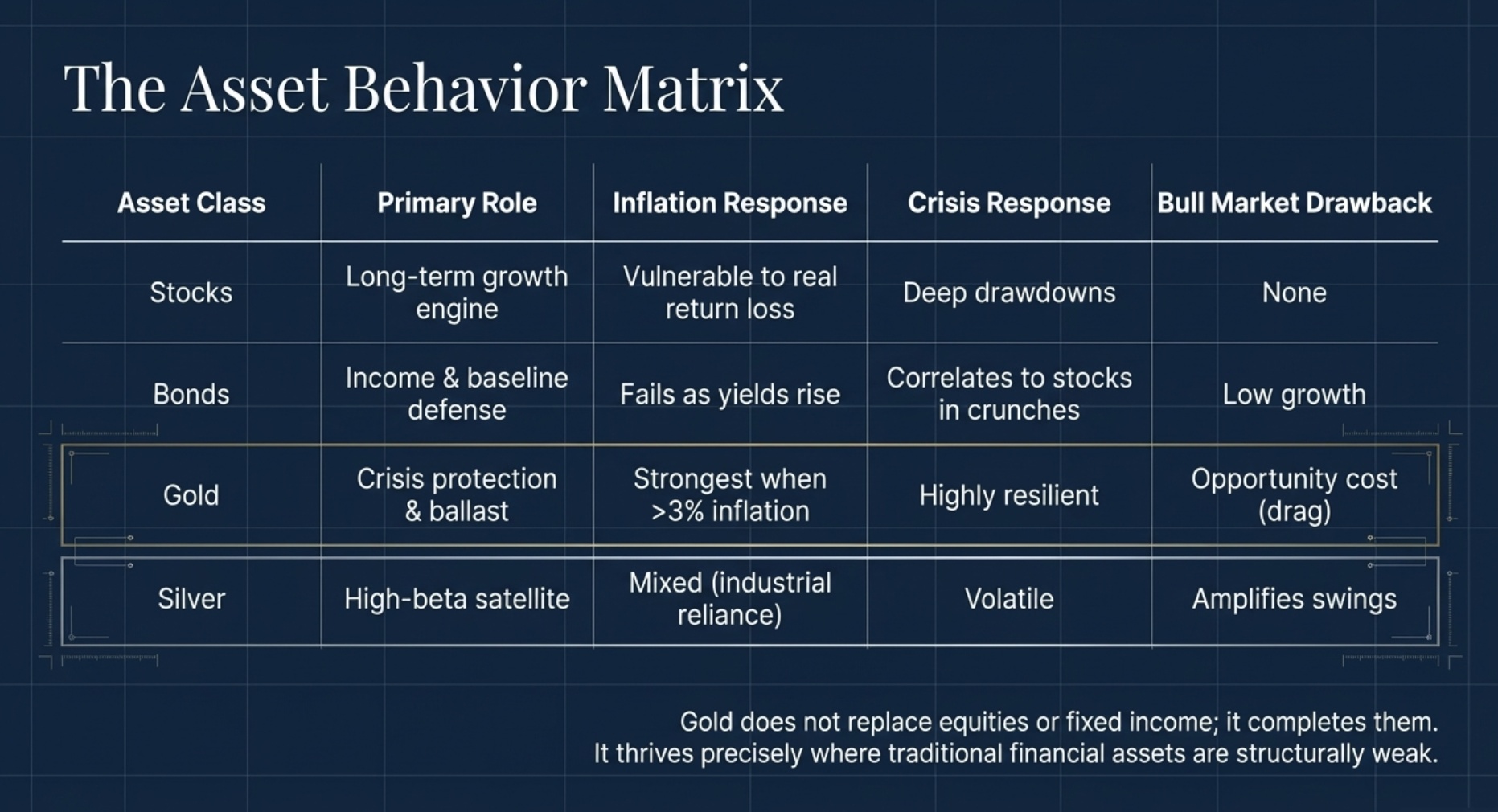

Gold vs stocks vs bonds

A simple way to think about roles:

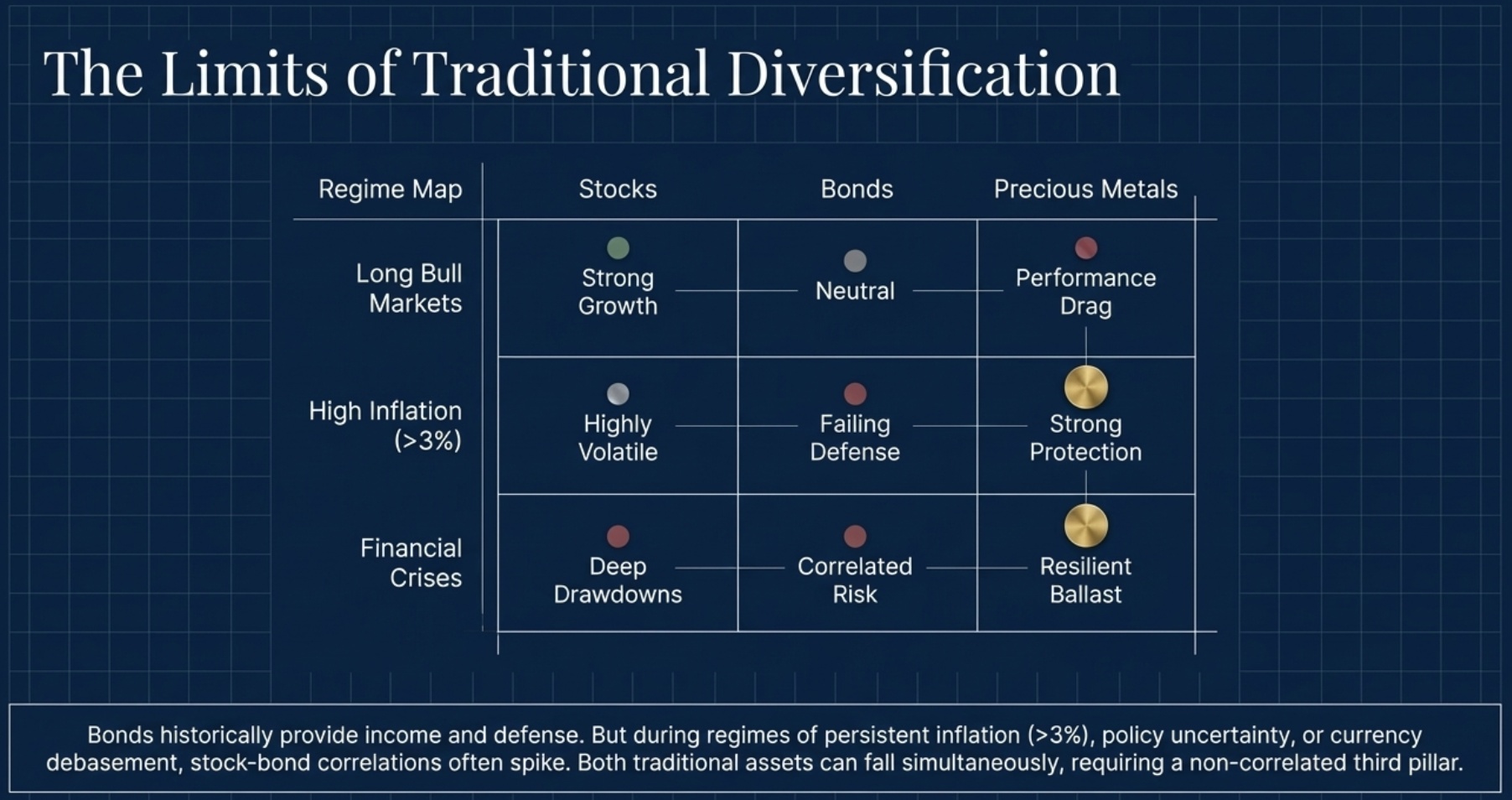

- Stocks: Primary driver of long‑term growth, but vulnerable to deep drawdowns and periods of poor real returns.

- Bonds: Historically provided income and diversification, but in high inflation or rising‑rate periods they can fall alongside stocks, reducing their defensive power.

- Gold: No yield, but offers crisis protection and low correlation; tends to hold or gain value when stock‑bond combinations are stressed, improving risk‑adjusted returns.

In other words, gold doesn’t replace stocks or bonds; it complements them by behaving differently when the usual “stocks up, bonds protect” pattern breaks down.

Liquidity, spreads, and time horizon

Before deciding how much gold and silver to own, weigh three practical constraints:

- Liquidity: How quickly you could turn metals into cash through reputable dealers if needed.

- Spreads: The difference between dealer buy and sell prices; a wider spread means a higher round‑trip cost if you buy and later sell.

- Time horizon: How long you realistically plan to hold metals before you might need the money. Longer horizons can better absorb volatility and spreads, while short horizons argue for smaller positions.

If you expect to need significant cash within a few years—for a house, education, or business—you may want a lower metals allocation or focus on particularly liquid products. For background on how products, pricing, and spreads work, it helps to start with a dedicated bullion investment guide.

How gold and silver behave in different scenarios

High inflation

In sustained high‑inflation regimes, gold has often protected purchasing power better than cash or long‑duration bonds. Historical analysis suggests gold’s inflation‑hedging power tends to show up more clearly over longer horizons and in periods where inflation is persistently above roughly 3%.

Silver’s response to inflation is more mixed: it can provide additional protection in some regimes, but its industrial demand and volatility make its behavior less consistent than gold’s. This is one reason many investors anchor their precious metals sleeve primarily in gold and treat silver as a smaller, higher‑beta component.

Financial crises and risk‑off shocks

During certain crises—credit stress, policy uncertainty, or stock‑bond correlations spiking—gold has often delivered positive or at least relatively resilient returns while both stocks and bonds suffer. That “ballast” effect is what many portfolio studies cite when they conclude that gold can improve risk‑adjusted returns in diversified portfolios.

The key nuance is that not every crisis is the same; sometimes liquidity crunches or forced selling can temporarily hit all assets. Over full cycles across multiple crises, however, gold has tended to behave differently enough from stocks and bonds to justify a modest strategic allocation.

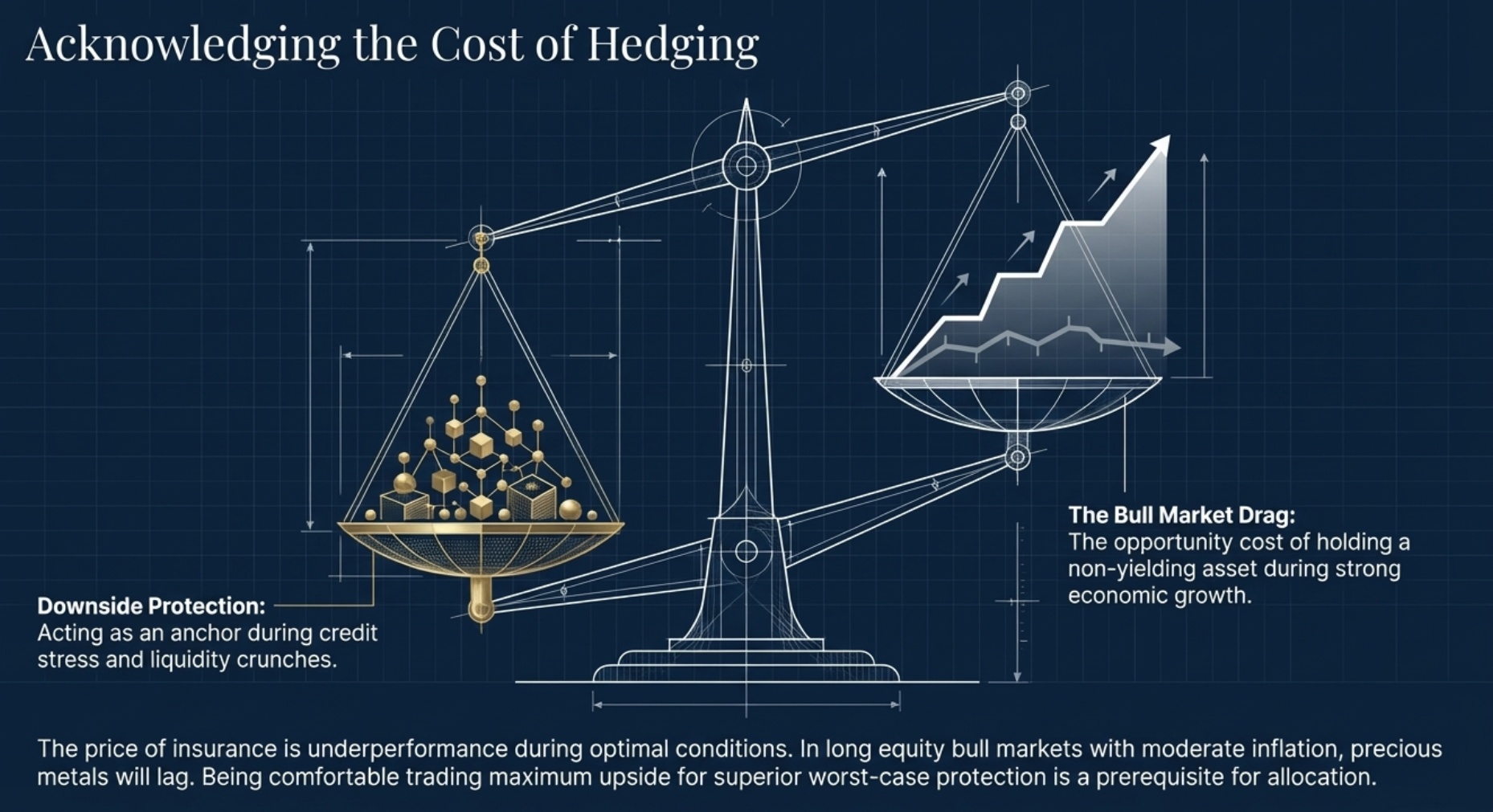

Strong equity bull markets

In long, strong equity bull markets with moderate inflation and rising real yields, gold and silver often underperform stocks. In those periods, a precious metals allocation can feel like a drag, because the hedge you bought is not “needed” when everything else is working.

That underperformance is the cost of holding a hedge: you’re trading some upside in the best times for better protection in the worst times. Being comfortable with that trade‑off is essential before you decide how much of your portfolio to devote to bullion.

For a product‑level view of how different coins and bars can express these roles, you can explore core bullion categories.

Typical allocation ranges

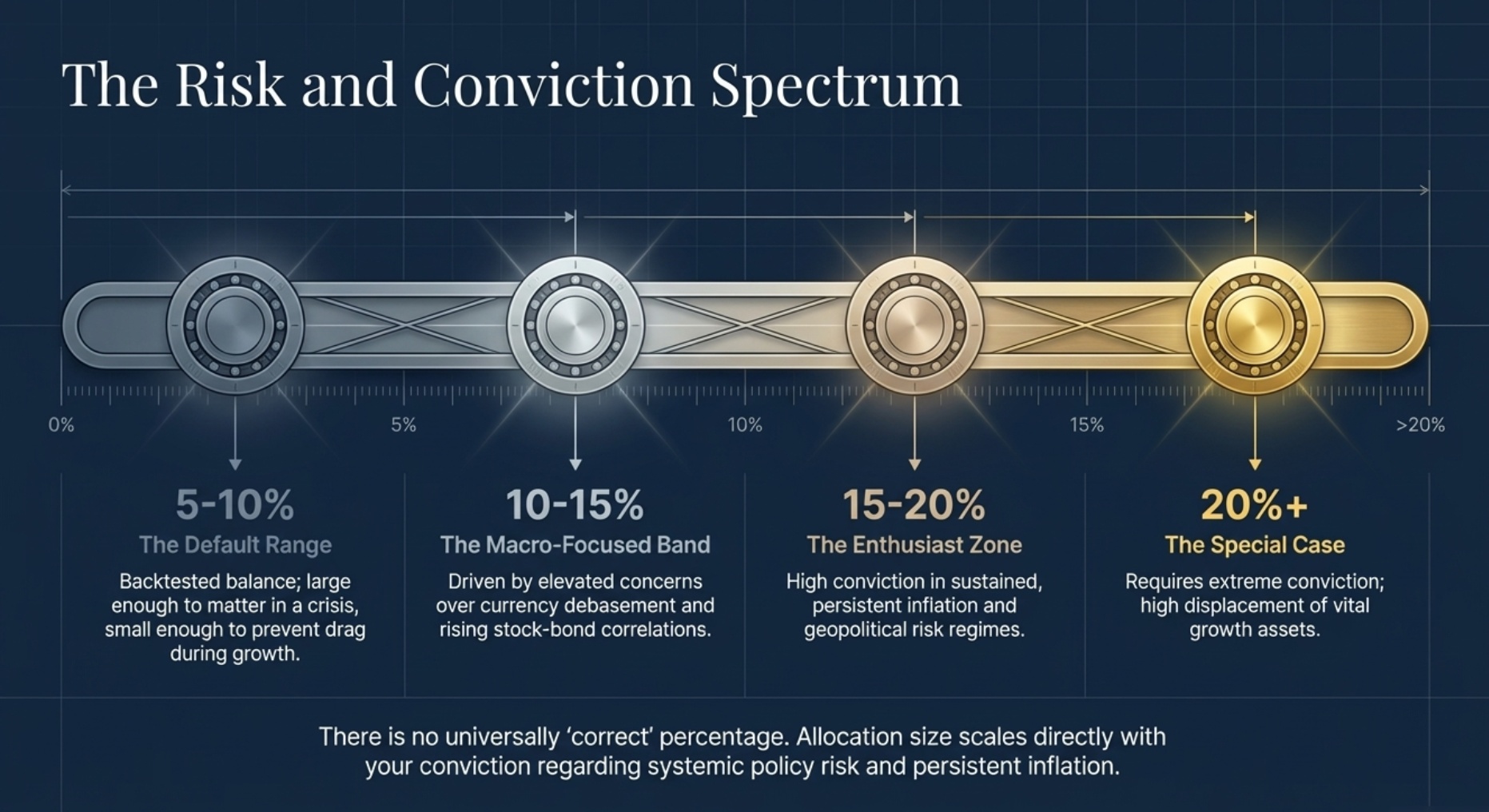

Why 5–10% shows up so often

The idea of putting around 5–10% of a portfolio into gold and silver shows up in many professional and retail guides because backtests often find that modest metals exposure can improve diversification without overwhelming the portfolio’s growth engine. That does not mean 7% or 9% is magically “correct,” only that somewhere in this neighborhood has historically balanced benefits and costs for many investors.

If you want a simple starting point, you might view 5–10% as a default exploration range: big enough to matter in inflation or crises, small enough that you remain primarily exposed to stocks and bonds for growth and income. You can then adjust up or down as you learn how metals fit your temperament.

When 10–15% or more might be reasonable

A number of macro‑focused investors and research pieces argue for 10–15% or thereabouts in gold (or broader metals) in an era where stock‑bond diversification looks less reliable. Evidence‑based studies highlight that portfolios including gold have sometimes achieved higher returns and lower drawdowns than traditional 60/40 mixes, thanks to gold’s behavior in stressed regimes.

Allocations above ~10% may make more sense if you are particularly concerned about:

- Persistent inflation and currency debasement.

- High policy uncertainty and geopolitical risk.

- Rising stock‑bond correlations eroding the classic 60/40 hedge.

Even then, 10–15% should be treated as a thoughtful upper band, not a “must hit” target, and should be considered in the context of your broader financial plan.

Why very high allocations are a special case

Allocations above 20% in precious metals can be appropriate for some individuals but are usually tied to strong convictions, unique circumstances, or very high overall net worth. They increase your exposure to metals’ volatility and to the opportunity cost of not holding other assets that may outperform over long stretches.

Instead of assuming that higher is always better, it’s more realistic to ask: “At what point does adding more metals stop significantly improving my downside protection and start displacing other things I really need in the portfolio?”. For many diversified investors, that inflection point appears somewhere in the mid‑teens rather than at extreme allocations.

Allocation vs risk profile

| Risk profile | Example metals share of portfolio | Example gold/silver split (within metals) | Notes |

|---|---|---|---|

| Cautious / income‑oriented | 3–7% | ~85% gold / 15% silver | Focus on stability and liquidity; minimal drag in long bull markets. |

| Balanced long‑term | 5–12% | ~70–80% gold / 20–30% silver | Aims for meaningful diversification without dominating the portfolio. |

| Risk‑aware, macro‑focused | 10–18% | ~65–75% gold / 25–35% silver | Stronger hedge against inflation and crises; more sensitivity to metals cycles. |

| Metals‑heavy enthusiast | 15–25%+ | Flexible, often still gold‑heavy | High conviction; significant opportunity cost and volatility. |

These bands are illustrative, not prescriptive. They’re meant to help you map your risk profile to a ballpark, then refine based on your own comfort and circumstances.

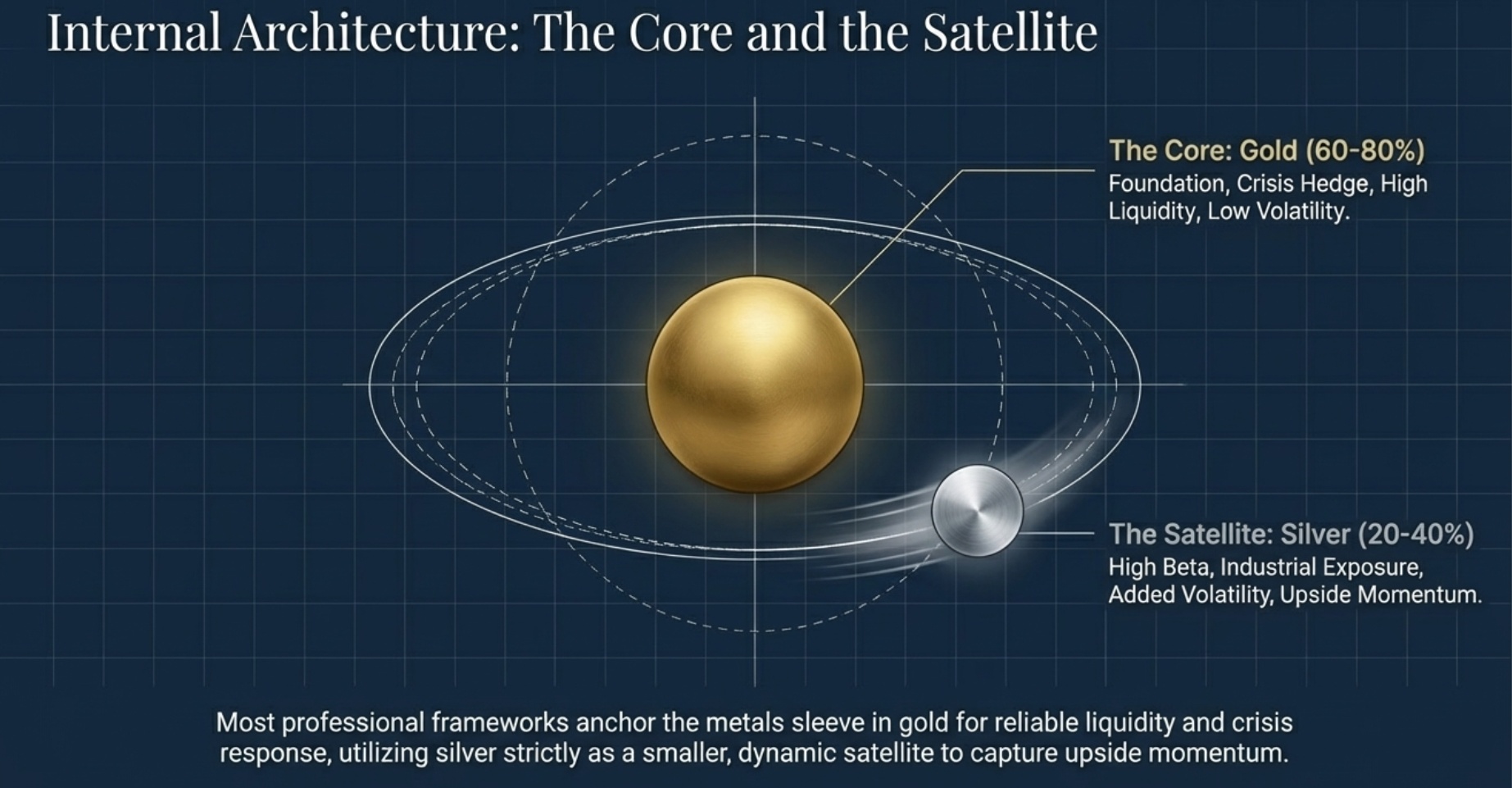

Balancing gold vs silver inside your metals sleeve

Direct answer: most investors make gold the foundation and use silver as a smaller satellite position.

Explanation: Gold’s role as a crisis hedge and its strong liquidity across dealers and jurisdictions make it a natural core holding, while silver’s industrial exposure and volatility can add upside but also bigger swings. Many frameworks therefore tilt 60–80% of the metals sleeve toward gold and allocate the remainder to silver, adjusting the mix with risk tolerance.

If you prefer to express that mix via different product types (coins vs bars, different sizes), a practical step is to review a bullion pricing and spreads guide so you understand how each choice affects entry cost and exit price.

Turning percentages into real numbers

Direct answer: once you pick a target percentage, multiply it by your total portfolio and then split that amount between gold and silver according to your chosen ratio.

Explanation: Suppose your portfolio is $120,000 and you aim for an 8–12% metals range. At 10%, that’s $12,000. If you choose a 70/30 gold/silver mix, you’re targeting about $8,400 in gold and $3,600 in silver over time. You can then map those dollar amounts into specific coins or bars that fit your budget and liquidity needs, building in stages rather than in one lump sum.

It’s also wise to look at what you already own—jewelry, inherited coins, existing bullion—and include those in your mental allocation so you don’t accidentally over‑concentrate in metals.

Building and maintaining your precious metals allocation

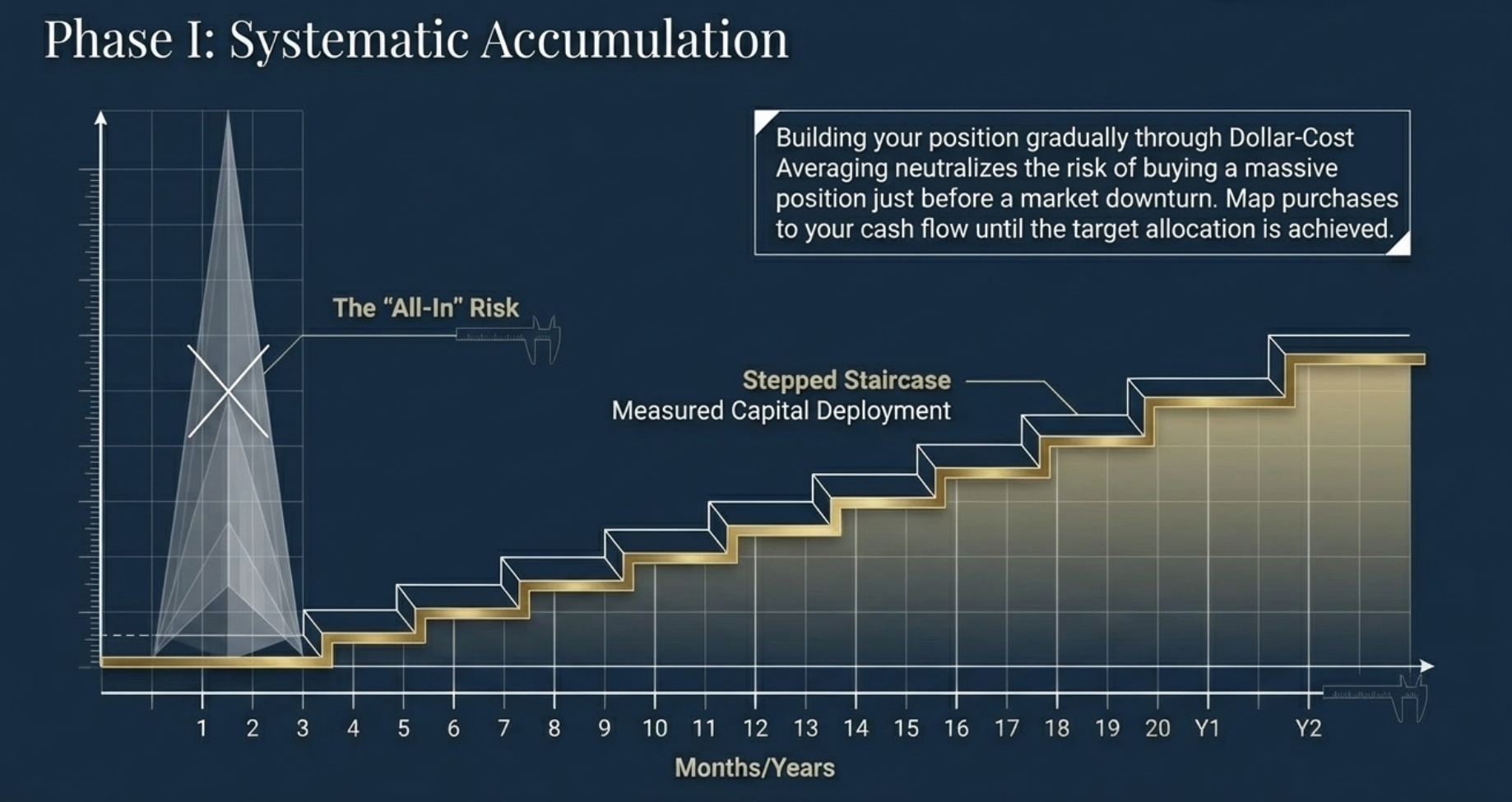

Build gradually instead of all at once

Direct answer: most investors are better served by building their gold and silver allocation gradually rather than going “all in” at once.

Explanation: Dollar‑cost averaging—spreading purchases over months or years—reduces the risk of buying a large position right before a downturn and makes it easier to match your allocation plan to your cash flow. You can, for example, commit a fixed amount every month until you reach your target range, then slow to maintenance purchases.

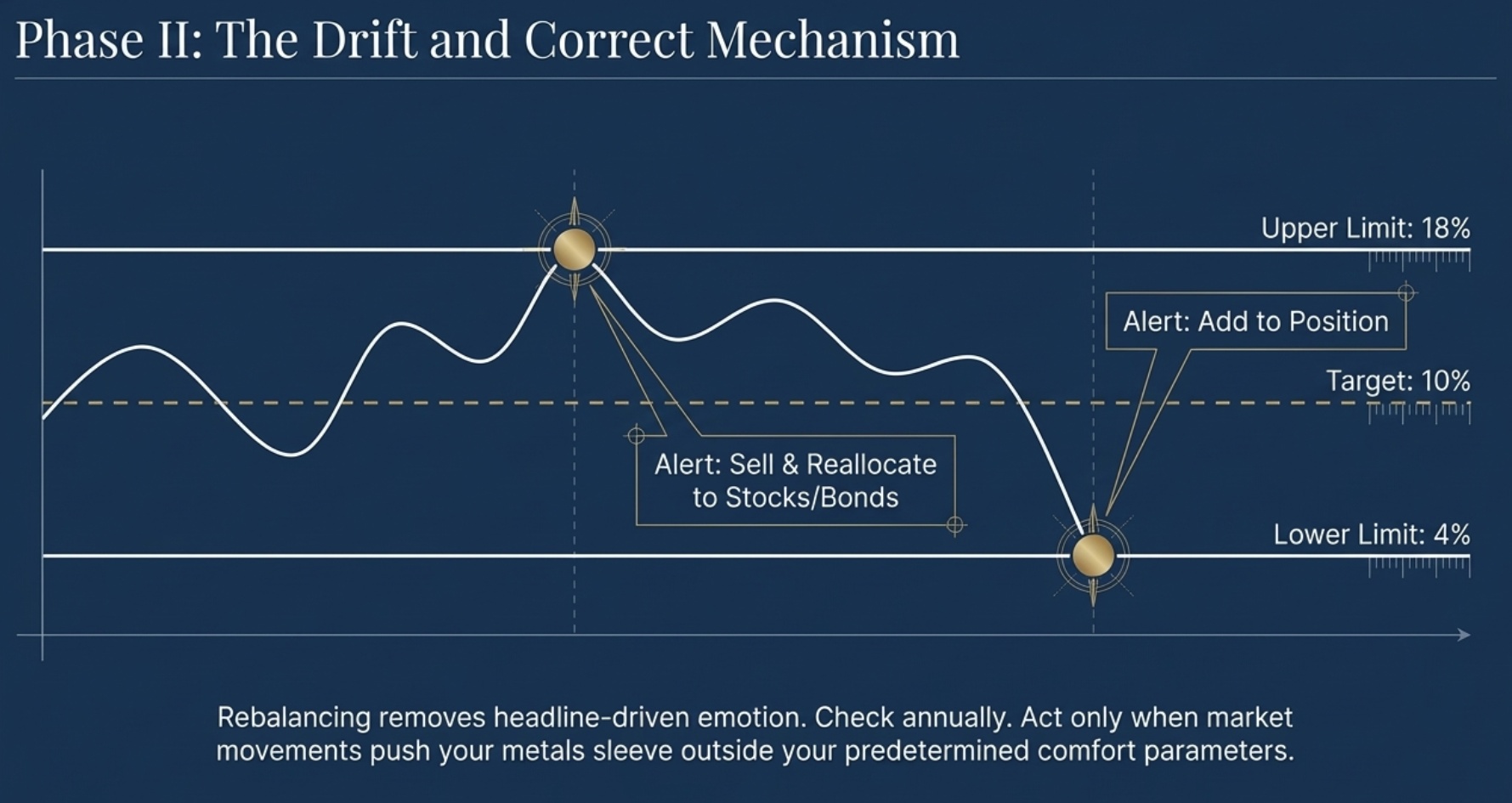

Rebalancing and staying within your range

Rebalancing is how you keep your metals sleeve aligned with your risk profile as markets move. If metals rally and grow to, say, 18% of your portfolio while your target band is 8–12%, you might sell part of the position and reallocate to underweight assets; if they fall to 4% and you’re comfortable around 10%, you might add.

Having a simple rule—like checking once a year and acting only when you drift beyond your band—helps you avoid making emotional, headline‑driven decisions.

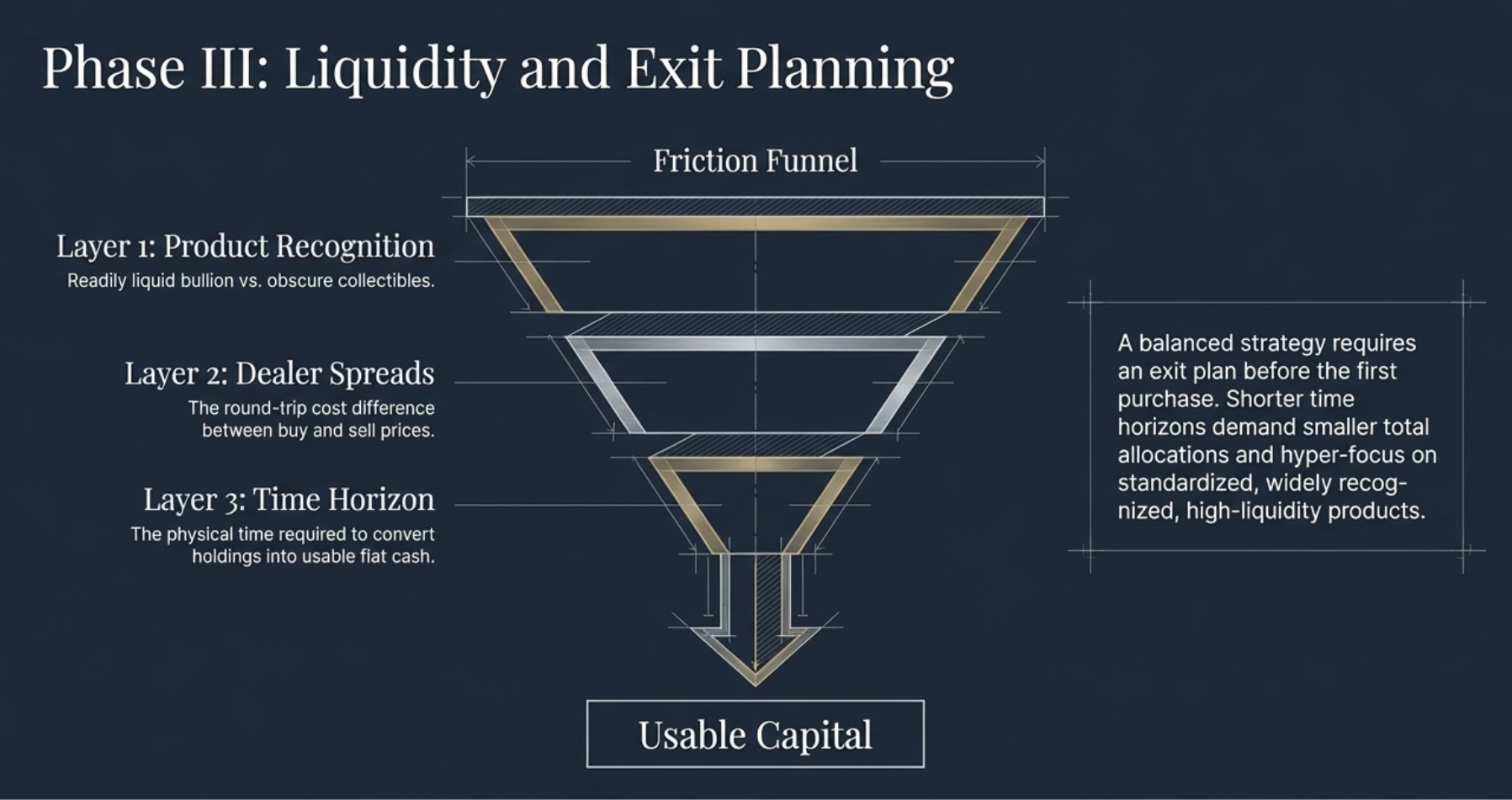

Liquidity planning and exit strategy

Direct answer: before buying, decide how you’d sell.

Explanation: A balanced strategy includes knowing which products are easiest to liquidate (typically widely recognized bullion coins and standard bars), which dealers you’d use, and roughly how long it would take to convert holdings into cash. Planning this upfront helps you avoid being forced into poor terms later because you need money quickly and hold only obscure or illiquid products.

You can also learn how local buyers structure offers—including how they apply spot, purity, and spreads—so you can approximate likely proceeds when planning rebalances.

Topic cluster: inflation, hedging, and diversification

If you want to go deeper on how a balanced precious metals strategy fits into a bigger financial picture, consider exploring related topics such as:

- Inflation and safe‑haven behavior: how metals tend to respond in different inflation regimes and why they often act as long‑term, not short‑term, hedges.

- Hedging with gold and other commodities: how gold compares to broader commodity exposures when protecting a stock‑bond portfolio.

- Diversification in practice: what correlation and drawdown data say about adding gold to traditional stock‑bond mixes.

On your own site, you can support this with a small content cluster: an inflation‑focused article, a diversification explainer, and a “mistakes to avoid when selling” piece, all internally linked from this allocation guide to give readers a complete journey.

FAQs: how much gold and silver is enough?

How much gold and silver should I have in my portfolio?

For many diversified investors, a modest metals sleeve in the 5–15% range is a practical starting point, not a rule. The right number depends on your risk tolerance, time horizon, and how big a hedge you want relative to growth assets.

What percentage of my portfolio should be in gold vs other assets?

Most portfolios still keep the majority in stocks and bonds, with gold and silver as a smaller diversifier, often single‑digit to low‑teens percentages. Within that sleeve, gold typically takes the larger share because of its stability and liquidity.

How do I decide how much silver to own compared to gold?

Use gold as the foundation and adjust silver based on your risk appetite; many investors keep silver at 20–40% of their metals allocation and let gold do the heavy lifting. If you want smoother behavior, tilt more toward gold; if you accept bigger swings, allocate a bit more to silver.

Is 5–10% in precious metals enough to diversify my portfolio?

For a lot of stock‑and‑bond portfolios, even 5–10% in metals has historically improved diversification and reduced some drawdowns. Going higher can add more hedge but also increases the cost of not holding other assets when they outperform.

Can I put too much of my portfolio into gold and silver?

Yes—very high allocations can leave you under‑exposed to income and growth, and overly reliant on metals cycles. Past a certain point, extra ounces add less to protection and more to opportunity cost.

Should I buy all my bullion at once or build my allocation over time?

Most investors are better off building over time with regular purchases, so they average into the market and keep decisions aligned with cash flow. That approach is easier to stick with than trying to guess the perfect moment.

How often should I rebalance my gold and silver allocation?

Checking once a year and acting only when you drift clearly outside your target band is enough for many people. The key is having any simple, written rule at all—and following it—rather than reacting to every headline.

If you are deciding how much gold and silver is enough for you, start by picking a realistic target range that matches your risk profile, then build toward it gradually with liquid products and a clear rebalancing plan. Once you have that framework, you can use education, simple math, and a reputable dealer to turn percentages on paper into a precious metals allocation that genuinely strengthens your overall portfolio.